A Private Market Solution to Flood Insurance: Reducing Federal Exposure through NFIP Reform

9 min read · Oct 8, 2025

Download issue here.

Executive Summary

For more than 50 years, the private insurance industry was unable to take on the flood peril, making the National Flood Insurance Program (NFIP) essential in reducing systemic risk. That is no longer the case.

The NFIP is $22.525 billion in debt (including a $2 billion increase in 2025), and every new policy sold adds risk to the U.S. taxpayer. This debt level would have been even higher if Congress had not forgiven $16 billion in 2018. The NFIP continues to take on risks that the private market is ready and better prepared to manage.

Neptune Flood recommends a practical shift:

- Continue offering renewals to existing NFIP customers. Current NFIP policyholders should be able to maintain their coverage for as long as they own their property.

- Stop selling new NFIP policies. The private market already has the tools, technology, and capacity to manage the risk that the NFIP continues to add. Unlike many legacy renewals, which are still capped on a glide path, new NFIP policies are charged the full Risk Rating 2.0 rate. Private insurers often offer lower premiums than the NFIP full-risk price.

- Maintain a small safety net. For the small group (about 5%) who can’t get private coverage after documented declinations, the NFIP would continue to serve as a last-resort option.

This transition could be implemented by the Administration without new legislation, as outlined in a FEMA memo that included the option to halt new NFIP enrollments.

The case for action is straightforward, and the benefits are clear:

Introduction

Flood insurance plays a critical role in keeping the housing market stable, protecting banks, and safeguarding millions of American homeowners. For more than 50 years, the National Flood Insurance Program (NFIP) has been the backbone of that system. But today, the program is $22.525 billion in debt (less than $8B away from its $30.43B borrowing authority) and continues to add new financial risk to the federal balance sheet.

This paper proposes a practical change: stop selling new NFIP policies, while continuing to allow renewals for existing NFIP policyholders. A narrow safety net would remain for the small number of applicants who cannot secure coverage in the private market.

This shift would not require new legislation. It would:

The transition could begin immediately. Based on standard insurance market patterns, about 430,000 to 540,000 properties each year would secure private coverage instead of new NFIP policies. At current rates, this translates to $550–700 million in premiums annually shifting into the private market, and we expect that most buyers would pay less than the NFIP’s full-risk price through private flood insurance platforms that can connect customers with a broad group of global insurance and reinsurance partners who should be able to absorb this flow.

A Two-Pronged Solution

1. Stop NFIP from Adding New Policies Nationwide

Under this proposal, FEMA would stop selling new NFIP policies nationwide. Homeowners purchasing flood insurance for the first time (or buying a new property) would turn to private insurers for coverage.

Importantly, renewals would continue for all existing NFIP policyholders. No current customer would be forced off their policy. They could maintain NFIP coverage as long as they own their property, and policies could still be assigned to a buyer when a home is sold, keeping real estate transactions running smoothly.

Pausing new NFIP enrollments could immediately prevent further growth of federal risk while ensuring that new buyers enter a competitive private flood insurance market, one that provides broader and more customizable coverage.

2. Establish a Narrow “Last Resort” Option

FEMA would maintain a tightly controlled fallback channel to ensure that even the hardest-to-insure properties can still obtain coverage, but only for applicants who cannot secure private insurance.

Here’s how it would work:

- Homeowners must first seek quotes from private carriers (“private-first” approach).

- Only after receiving two documented declinations would they become eligible for a new NFIP policy.

This ensures NFIP functions strictly as a safety net of last resort, not as a competitor to private insurers. The safety net would be deliberately narrow (about 5% of potential new policies at most) and designed to be auditable to prevent abuse. The federal government has unique capabilities to manage the most severely exposed properties, a role that would complement private carriers by addressing extreme residual risks in the public interest.

Importantly, every policy issued through this pathway would still be priced at a full-risk, actuarially sound premium under FEMA’s Risk Rating 2.0 system. That means even these last-resort policies do not burden taxpayers with underpriced risk.

This model is not unprecedented. It mirrors state-level programs like Florida’s Citizens Property Insurance Corporation, which provides coverage only when private carriers cannot. It’s a proven approach that balances the need for a public backstop with the efficiency and innovation of the private market.

Why Act Now

1. Reduce Federal Balance Sheet Risk Rapidly

The NFIP currently carries $22.525 billion in debt, including an additional $2 billion borrowed in February 2025. Continuing to issue new policies only compounds this liability, while pausing new enrollments immediately prevents further exposure, without disrupting coverage for existing policyholders.

As Figure 1 shows, NFIP claims have surged over time: 84% of total payouts occurred between 2005 and 2024, with over 36% concentrated in just the last eight storm seasons. This trend underscores a troubling reality: in an era of more frequent and severe storms, the federal government has proven unable to price flood risk accurately. The result is a growing burden on U.S. taxpayers.

Figure 1. NFIP losses over time, 1979-2024

2. Fair and Adequate Pricing

Under FEMA’s Risk Rating 2.0 system, new NFIP customers already pay the full risk-based premiums, with no subsidies. In contrast, many long-time policyholders are still shielded by annual caps of up to 18 percent, which keep their rates below actual risk levels. This creates an uneven playing field where new buyers often face NFIP quotes that are higher than private market options.

The private market avoids these distortions. Free from federal cross-subsidies and political limits, private insurers can set actuarially sound rates that reflect actual exposure and reward homeowners who invest in mitigation. Neptune’s analysis shows that up to 60% of new NFIP policyholders would pay less in the private market, often with broader coverage. This reform eliminates outdated competition with the NFIP and allows consumers to benefit from fair, market-driven pricing.

3. Harness Private Market Capacity

The private reinsurance industry now has record levels of capital available to cover flood risk, with global capacity at about $715–720 billion in 2024, and further growth into 2025. On top of that, catastrophe bonds add nearly $50 billion in additional protection (as of Q1 2025), creating a strong financial backstop.

Global investors view U.S. flood as an insurable and diversifiable risk, and private insurers have already expanded rapidly to meet this demand. Redirecting new policies into the private market would tap this deep pool of capital, ease the burden on taxpayers, and give homeowners access to broader and more flexible protection.

The private sector is both ready and eager to take on more flood risk, an opportunity long constrained by NFIP’s dominance.

4. Cutting-Edge Technology and Innovation

Private insurers bring precision tools that the NFIP cannot match. Advances in data science, from high-resolution flood models to machine learning, allow property-level risk assessment.

Private coverage also exceeds NFIP’s limits, offering higher caps and added protections, often at more competitive prices. A private-first system delivers innovation directly to homeowners, adapting faster than any government program.

5. Continuous Coverage Immune from Shutdowns

The NFIP’s authority relies on periodic congressional reauthorizations, and political standoffs have led to several lapses and 33 extensions since 2017 (as of October 2025). Each lapse temporarily halted the program’s ability to issue or renew policies, disrupting the housing market and leaving families without vital flood protection at critical times. During one lapse in June 2010 alone, 47,000 home sales were delayed.

Private insurers face no such disruptions. By moving new policies to the private market, homeowners gain stable, uninterrupted access to coverage regardless of political gridlock. This reform removes flood protection from the cycle of shutdowns and ensures that when storms threaten, insurance is always available.

Quantifying the Shift

To understand the annual impact of this change, we look at contracts in force (CIF), which count buildings covered and avoid double-counting condo units that can inflate the “policies in force” number. As of July 2025, there are 3,589,213 CIF, rounded here to about 3.59 million.

In the insurance world, policies are constantly renewing, expiring, or switching carriers. Using standard retention rates for the property and casualty industry (typically in the low to mid-80% range) means that 12–15% of policies turn over each year. Applying that to 3.59 million contracts, we estimate that 430,000 to 540,000 buildings annually would shift to the private marketinstead of entering NFIP as new policies.

For premiums, the benchmark is NFIP’s full-risk price. Based on the Government Accountability Office (GAO) data, the median Risk Rating 2.0 premium is $1,288 per policy (as of July 2023). Multiplying this by the number of policies shifting yields $550–700 million in premiums redirected to the private market each year.

Figure 2. Key Metrics of the NFIP Policy Transition

Over time, this steady transition would naturally shrink NFIP’s role. Within about seven years, NFIP would be reduced to a smaller “last resort” program, covering only the hardest-to-insure properties, roughly 150,000 to 200,000 policies nationwide (as shown in Figure 3).

Figure 3. Portfolio Transition to Private Market

Consumer Impact

For new buyers, the relevant pricing benchmark is the full-risk NFIP price under Risk Rating 2.0. Relative to that full-risk amount, we believe most policyholders would pay less in the private market today, while keeping lender compliance with policies that meet statutory equivalency.

A transition to the private market also improves quality protection. The NFIP’s standard residential limits have been unchanged for decades at $250,000 for building coverage and $100,000 for contents, which has not kept pace with home values or rebuild inflation and leaves many properties underinsured. Private flood policies can match or exceed NFIP form limits and frequently offer higher limits and optional coverages that matter to families and lenders, such as additional living expenses (loss of use), broader contents and basement coverage, and customizable deductibles. These enhancements are available at equal or lower premiums relative to the NFIP full-risk price for many risks, providing more complete financial protection during loss events.

Current NFIP policyholders would remain protected under their current NFIP policies and, for those not yet at their full Risk Rating 2.0 price, remain on a glide path with 18% annual price increases. This removes friction and any perceived instability in the housing market, while also allowing those policyholders to explore private market policies if they wish.

Legal and Operational Feasibility

1. Clear Authority

FEMA already has the authority to stop issuing new NFIP policies while allowing renewals to continue. This action does not require new legislation or lengthy rulemaking, making it an immediate, practical step the Administration can take.

2. No Impact on Current Policyholders

Existing NFIP customers would see no disruption. They could continue renewing their policies at current terms, and assignment of policies at property sale would remain in place, ensuring home transactions are not delayed.

3. Rapid Implementation

This shift can be executed within 90 days. FEMA would issue bulletins to Write Your Own carriers and NFIP Direct, set clear standards for documenting declinations under the last-resort channel, and create a simple reporting dashboard to track results.

FEMA as Last Resort and Market Regulator

This plan would redefine FEMA’s role in flood insurance in a way that plays to its strengths and reduces strain on taxpayers. Instead of acting as the nation’s primary flood insurer, FEMA would operate as a last-resort backstop and market regulator, while private carriers take on the vast majority of risk. This change can be made quickly through administrative action, without waiting for Congress.

Within 90 days, FEMA could direct Write Your Own carriers to stop issuing new NFIP policies, publish standards for documenting declinations, and set up a simple dashboard to track usage of the safety-net channel.

Under this framework, NFIP’s new business would be limited to properties that private insurers decline, with all policies priced at full-risk rates under Risk Rating 2.0. That ensures taxpayers are not subsidizing coverage and positions NFIP as a residual market program, similar to state FAIR plans or Citizens in Florida. Freed from the burden of insuring millions of homes, FEMA could focus its resources on managing high-risk cases, investing in mitigation, supporting low-income households, and providing data and oversight to guide the private market. This is a more sustainable role for government, leveraging public resources where they are most needed while allowing innovation and capital from the private sector to drive growth.

Conclusion

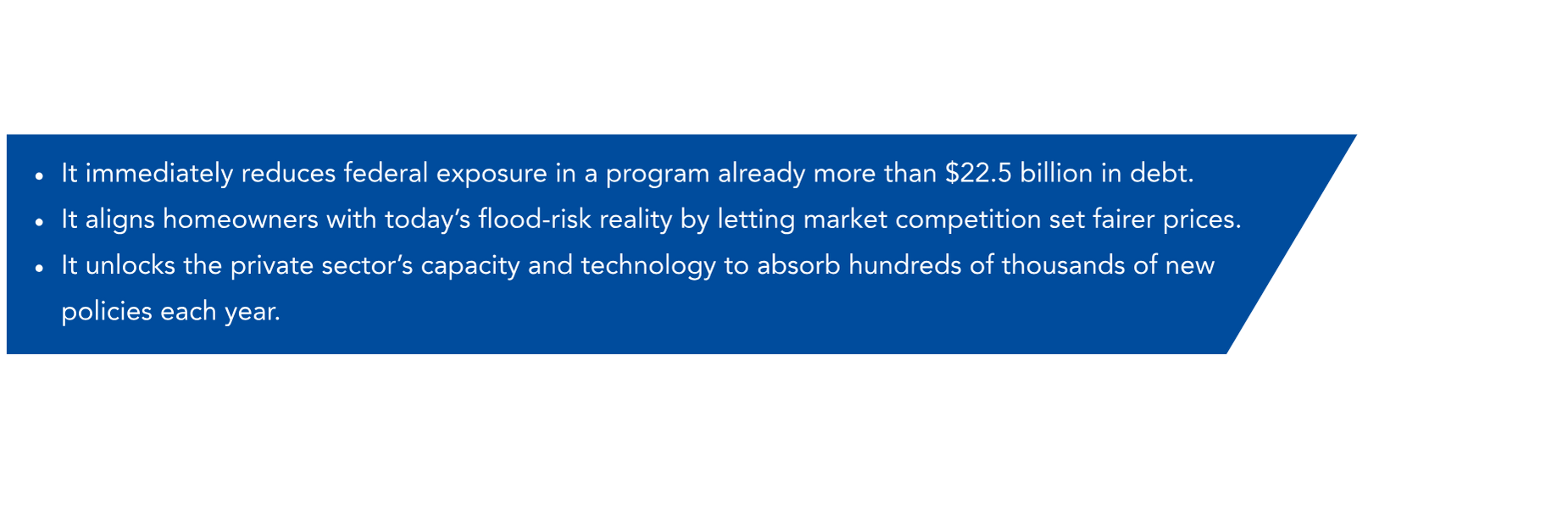

Ceasing NFIP’s sale of new policies while preserving renewals and a last-resort channel delivers three clear benefits.

The transition would be orderly, unfolding over six to seven years, with current NFIP policyholders fully protected and homeowners nationwide gaining more options and stronger coverage. This approach requires no new legislation, only decisive administrative leadership. At a moment when federal budgets are strained and flood losses are accelerating, maintaining the status quo is too risky.

The private market is ready, the tools exist, and the blueprint is clear. Now is the time to act before the next major storm arrives to build a safer, more resilient system that effectively spreads risk, protects families, and ensures coverage is always available when Americans need it most.